Summary

The Black Sea region is a significant supplier of agricultural commodities to the world. Over the past year, global grain and oilseed markets have been roiled by Russia’s ongoing war in Ukraine. Initially Ukraine’s grain and oilseed exports via sea routes were entirely cut off but have since been able to flow, facilitated by the United Nations through the Black Sea Grain Initiative. Meanwhile, the European Union has become a key importer and transshipment point for Ukrainian grains under the “Solidarity Lanes” initiative, including the Black Sea port of Constanta in Romania. Yet the most prominent exporter in the Black Sea region is Russia, from which strong exports continue to flow in 2022/23 and is forecast to reach a record for annual wheat exports. Despite the Russian government claims of export challenges, Russia’s grain and oilseed exports have thrived during the current marketing year with ample supplies and competitive prices. Export volumes could be even larger, but the Russian government continues to apply export taxes and quotas, trade-restricting measures that are self-imposed.

Large 2022/23 Russia Production and Stocks

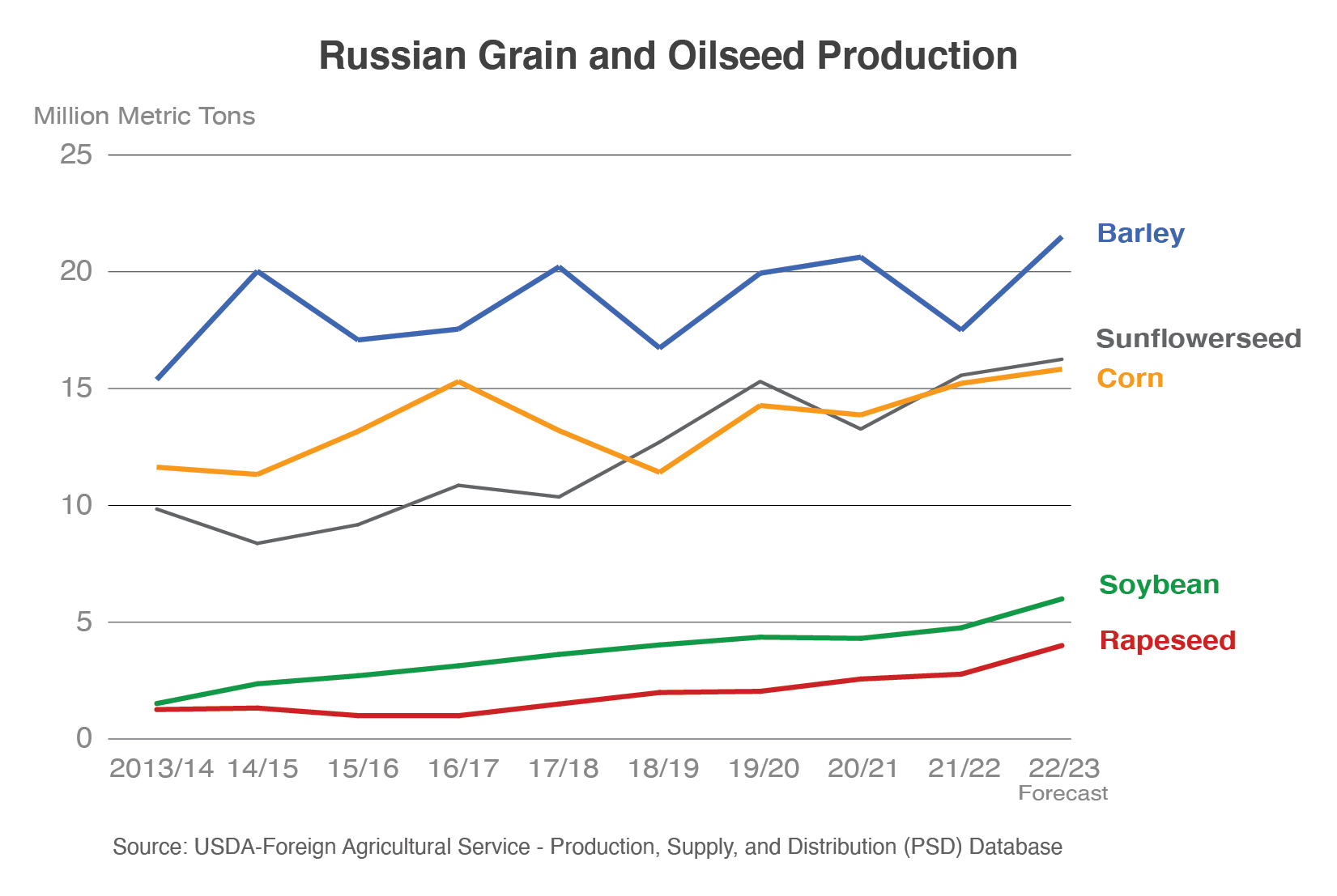

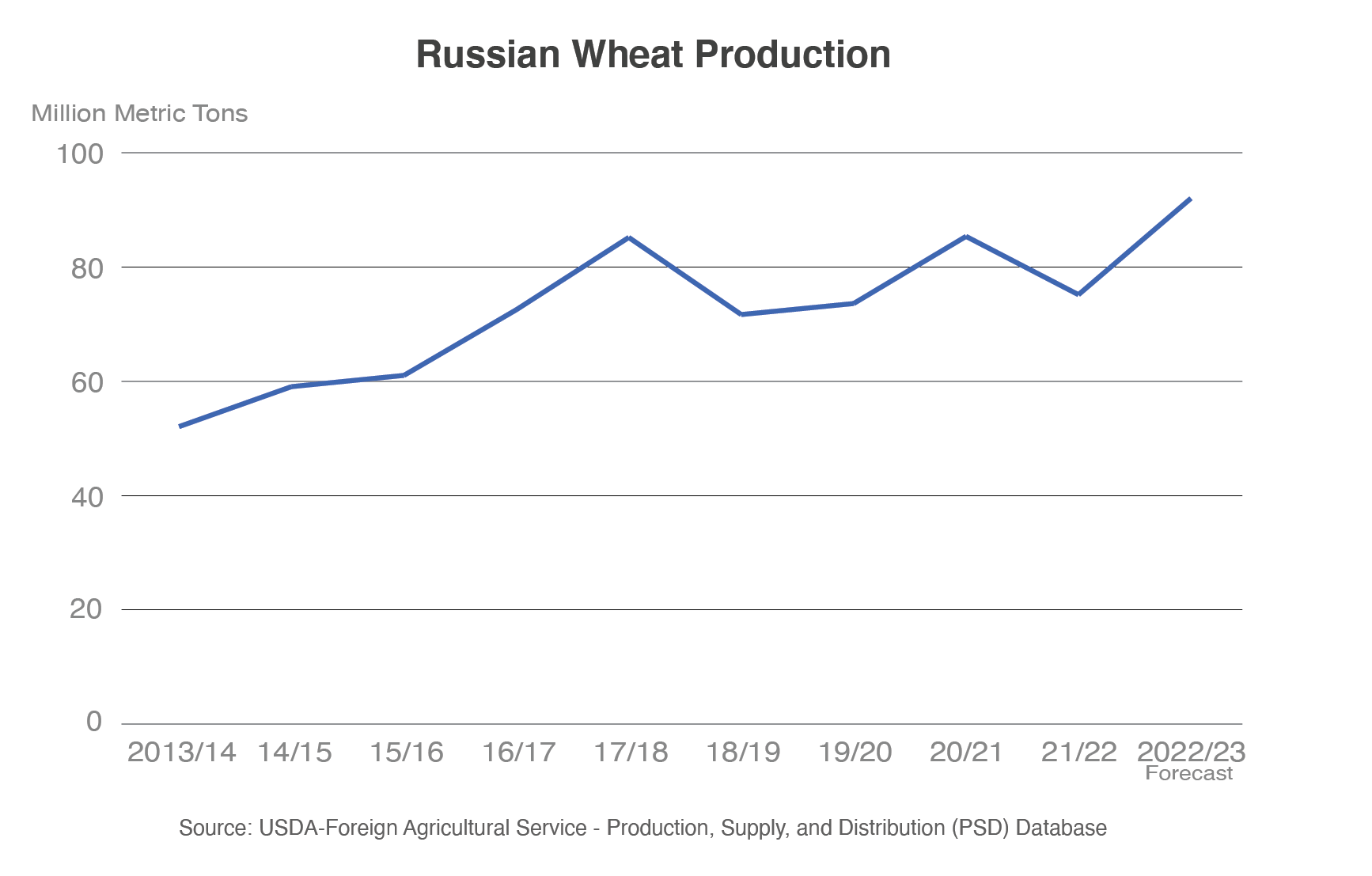

Over the past decade, Russian production of grains and oilseeds has increased significantly due to both expansion of area for some crops and improved yields for others. In 2022/23, production increased for all major grains and oilseeds. In fact, Russia had record production of wheat, sunflowerseed, and rapeseed. Both barley and wheat are primarily winter crops that had been negatively affected by an ice crusting event in 2021/22 but rebounded with ideal weather conditions in 2022/23. Wheat production has nearly doubled from a decade ago.

The expansion of Russian grain and oilseed production in 2022/23 is due to both an increase in planted area for all crops (except corn and sunflower seed) as well as increased yields for all of these commodities (with records for all commodities except sunflower seed, which was the second largest on record).

Notably, the USDA estimate of Russian wheat production only includes the wheat produced within the Russian Federation and does not include Ukrianian territory Russia has illegally attempted to annex, such as Crimea. USDA estimates Russian production at a record but lower than the Rosstat record estimate, which sets yields far above the previous record yields for both winter and spring wheat. See Russia Wheat: Record MY 2022/23 Harvest April 2023 Commodity Intelligence Report and High Russian Corn Crop Despite Delayed Harvest article in the April 2023 World Agricultural Production report for further details on the Russian wheat and corn crops, respectively.

In addition to production gains, Russia began 2022/23 with ample stocks of wheat. Stock levels were larger than normal because of export restrictions imposed by the government during the previous marketing year to ensure sufficient domestic supplies and maintain lower domestic prices.

Expanded 2022/23 Russian Grain and Oilseed Exports

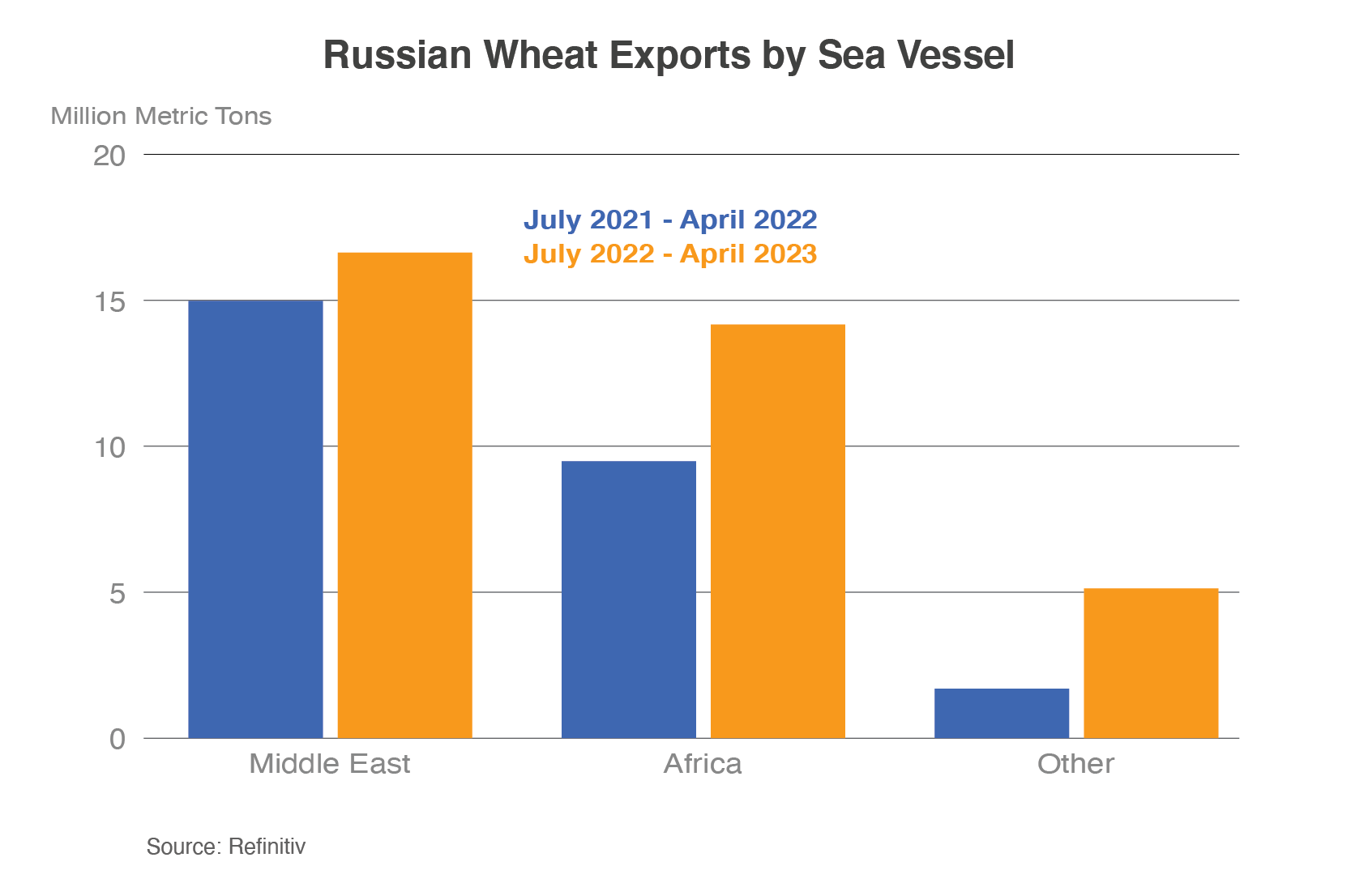

Actions by the Russian government has made it more challenging to ascertain precise export volumes and values over the past year. Russia ceased publishing its customs data in March 2022, meaning the latest publicly available statistics are through January 2022. Therefore, USDA uses alternative sources of data to track exports of grains and oilseeds from Russia. Port loading and vessel data provides one source of information by compiling information about vessels destination. The chart on the right shows the increase in wheat exports to the Middle East, Africa, and other countries for the first 10 months of the marketing year for 2022/23 compared to the prior year.

USDA also uses reported import data from key trading partners to monitor the exports of Russian grain and oilseeds exports. Many of Russia’s trading partners’ data show robust exports that occurred after Russia stopped publishing its data. Historical data from the past few years show some of the consistently large export markets for grains including Egypt, Turkey, Saudi Arabia, Iran, Kazakhstan, and Nigeria. Top sunflowerseed oil markets include China, Turkey, and Egypt and top markets for sunflowerseed meal markets include Turkey, the EU, and Belarus. Many of these countries have reliable, accessible trade data. For example, Turkey is a key trading partner for wheat and sunflowerseed meal. Data through February 2023 highlight Russia’s continued strong exports and expanding market share.

Russian wheat exports are forecast to hit a record 45.0 million tons in 2022/23, up 36 percent from the prior year and 3.5 million tons above its previous record in 2017/18. This is well above the next largest exporter with EU wheat exports at 35.0 million tons.

Monthly volumes of Russian wheat exports by sea range between 2.0 to 4.5 million tons during the current marketing year, averaging around 3.5 million tons. The top markets for sea-bound vessels have been Turkey, Egypt, Iran, Saudi Arabia, Sudan, and Algeria.

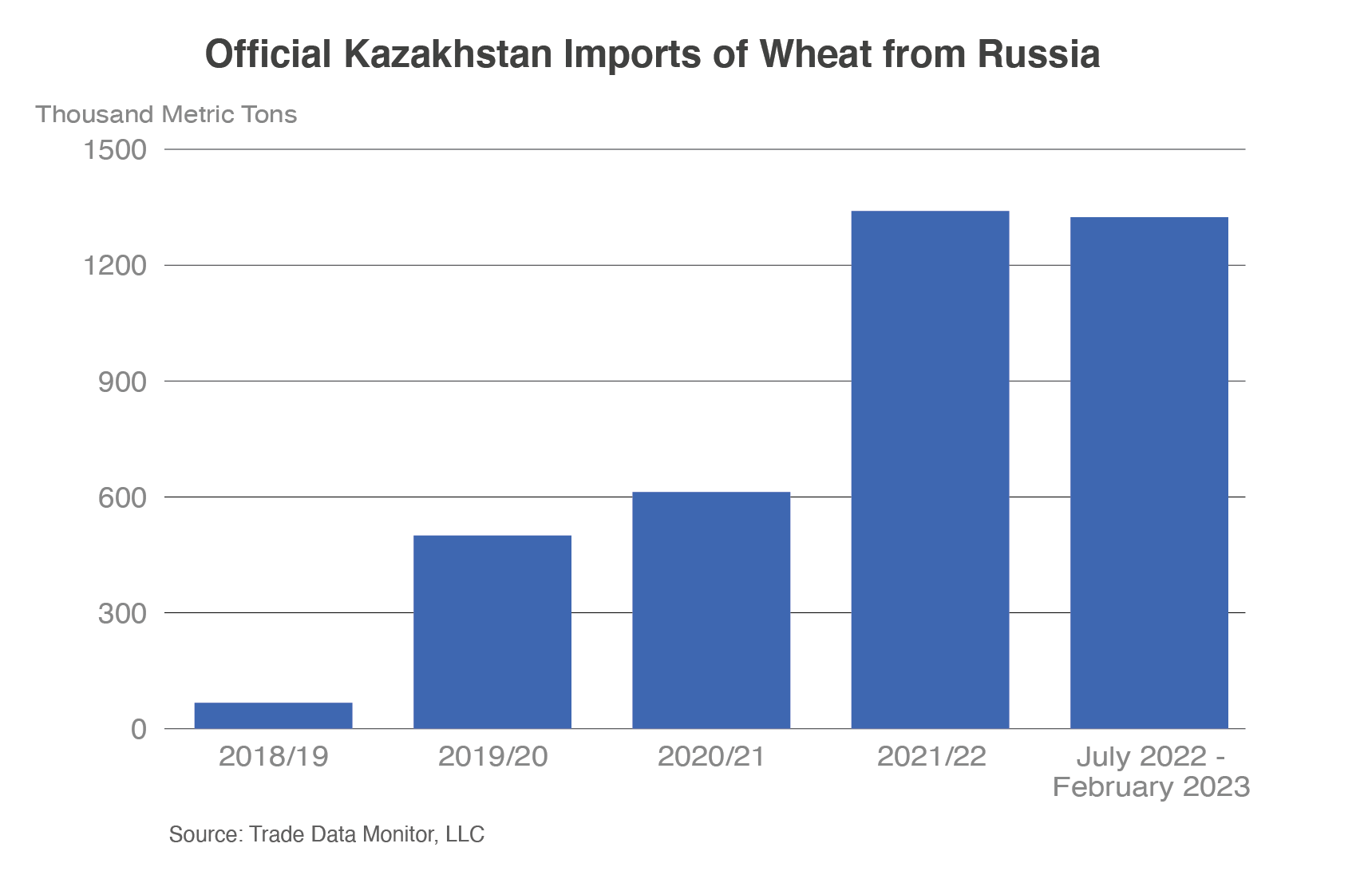

The vessel data do not fully capture exports via land transportation routes (truck or rail). Russia has shipped significant quantities to Eurasian Economic Union countries, principally Kazakhstan. Reported data from Kazakhstan Customs Control Committee show imports of Russian wheat nearly on par for July 2022 through February 2023 with imports for all of 2021/22. These volumes are up sharply from recent years as Kazakhstan has become a major trading partner. Kazakhstan is traditionally an exporter of wheat and wheat flour to the Central Asian region. However, in 2021/22, Kazakhstan had a reduced crop, necessitating imports to offset the shortfall. In 2022/23, Kazakhstan’s production was much larger but has continued to import price-competitive Russian wheat. Recently, the Kazakhstan government imposed a 6-month ban on imports of wheat by road, aimed at halting imports of low-priced Russian wheat by truck.

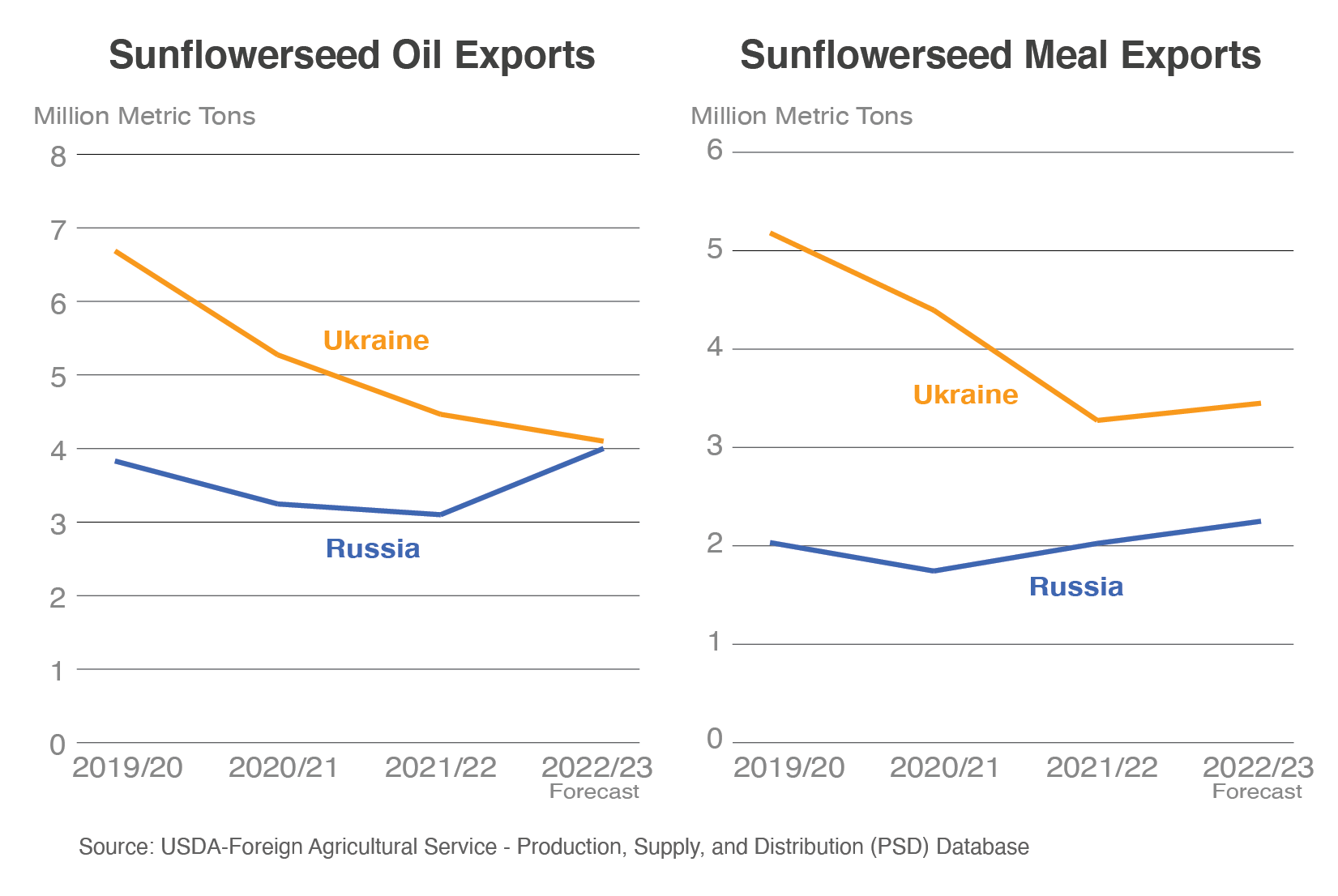

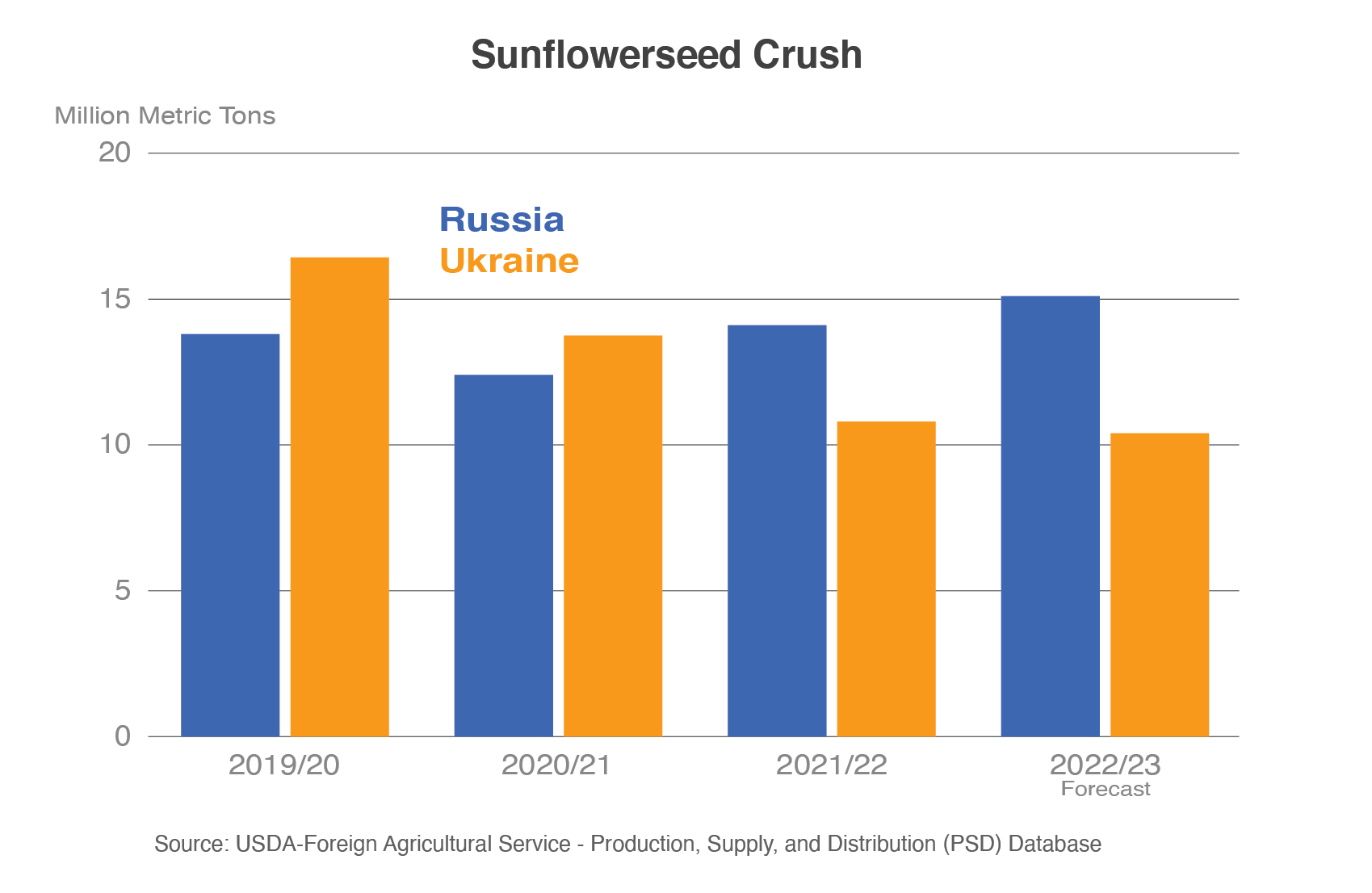

Russian exports of oilseed products are also higher. Domestic processing for oilseeds, particularly crush for sunflowerseed, has expanded in Russia despite flat domestic demand. Russia and Ukraine are historically the primary global exporters of sunflowerseed and products. Through processing (or crushing) sunflowerseeds, both sunflowerseed oil and sunflowerseed meal are produced. These products are largely exported to the Middle East and Asia. With a reduction in the availability of functional crushing facilities in Ukraine, Russia has expanded production of these value-added products for export markets.

Russian Export Prices Remain Competitive

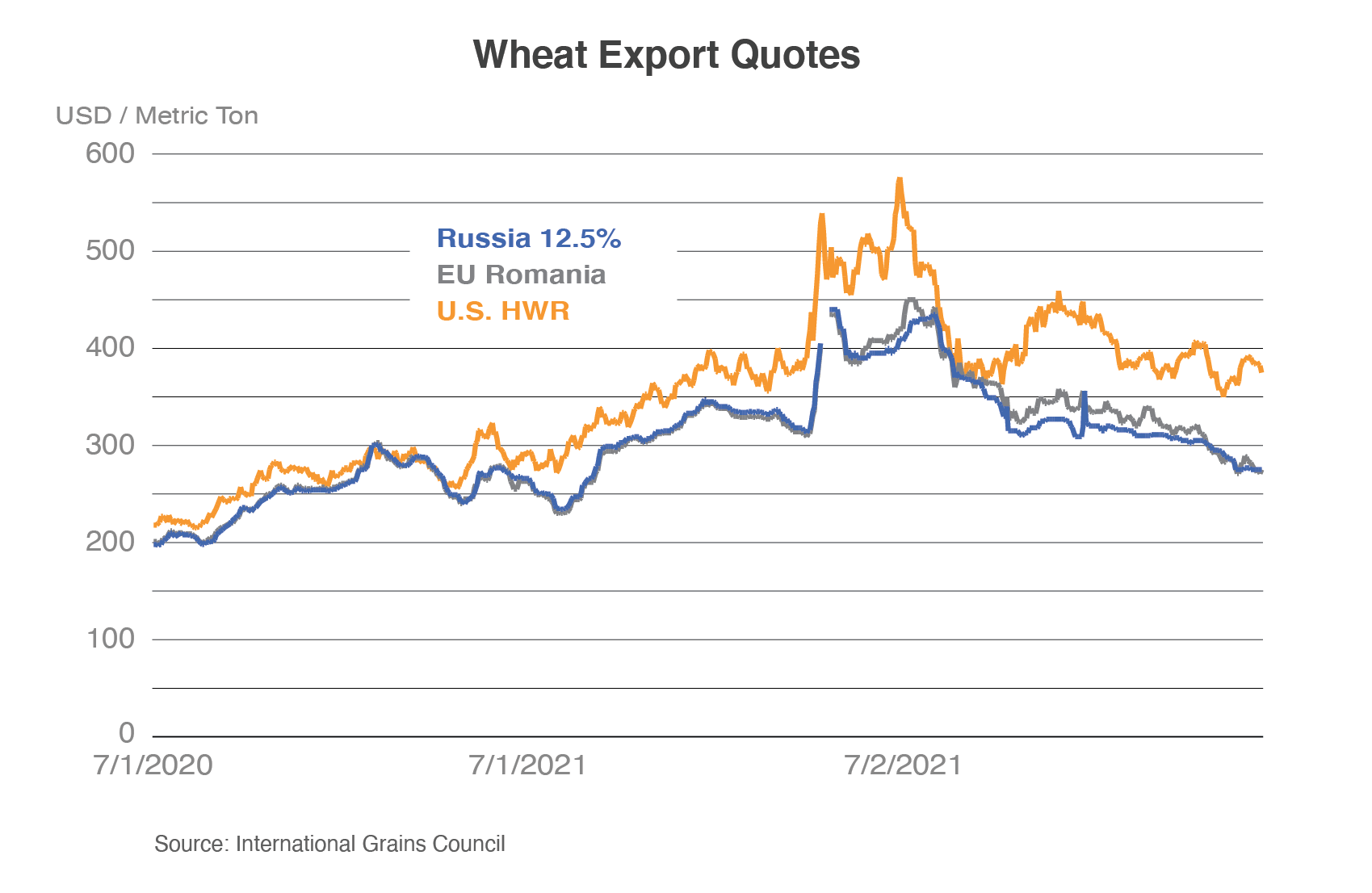

Russian wheat exports have been robust during 2022/23 due to competitive prices for most of the marketing year that began in July 2022. Over the past decade, the Black Sea region has emerged as the most competitive wheat supplier, and as a result, many countries in Africa and Asia have come to rely upon the region for both milling and feed-quality wheat. The key exporters from the Black Sea region include Romania, Ukraine, and Russia, and their quotes are generally lower than U.S. Hard Red Winter wheat, a mid-protein wheat than had a smaller crop due to drought this year. Ukrainian quotes were unavailable for the period when its ports were inaccessible, but now its export quotes are below Russian and Romanian quotes. However, free on board (F.O.B.) quotes do not include insurance and freight, which are reportedly high for Ukraine. Russia’s price advantage has enabled it to capture a large market share within Turkey and Egypt, two of the top three global importers.

Russia Restricting Its Own Exports

Over the years, Russia has used a variety of trade-restrictive measures to ensure domestic food security. While recent Russian government statements have claimed that economic sanctions have hampered Russia’s ability to export, in the case of grains and oilseeds, the Russian government itself has applied export taxes and quotas that affect its prices and export volumes.

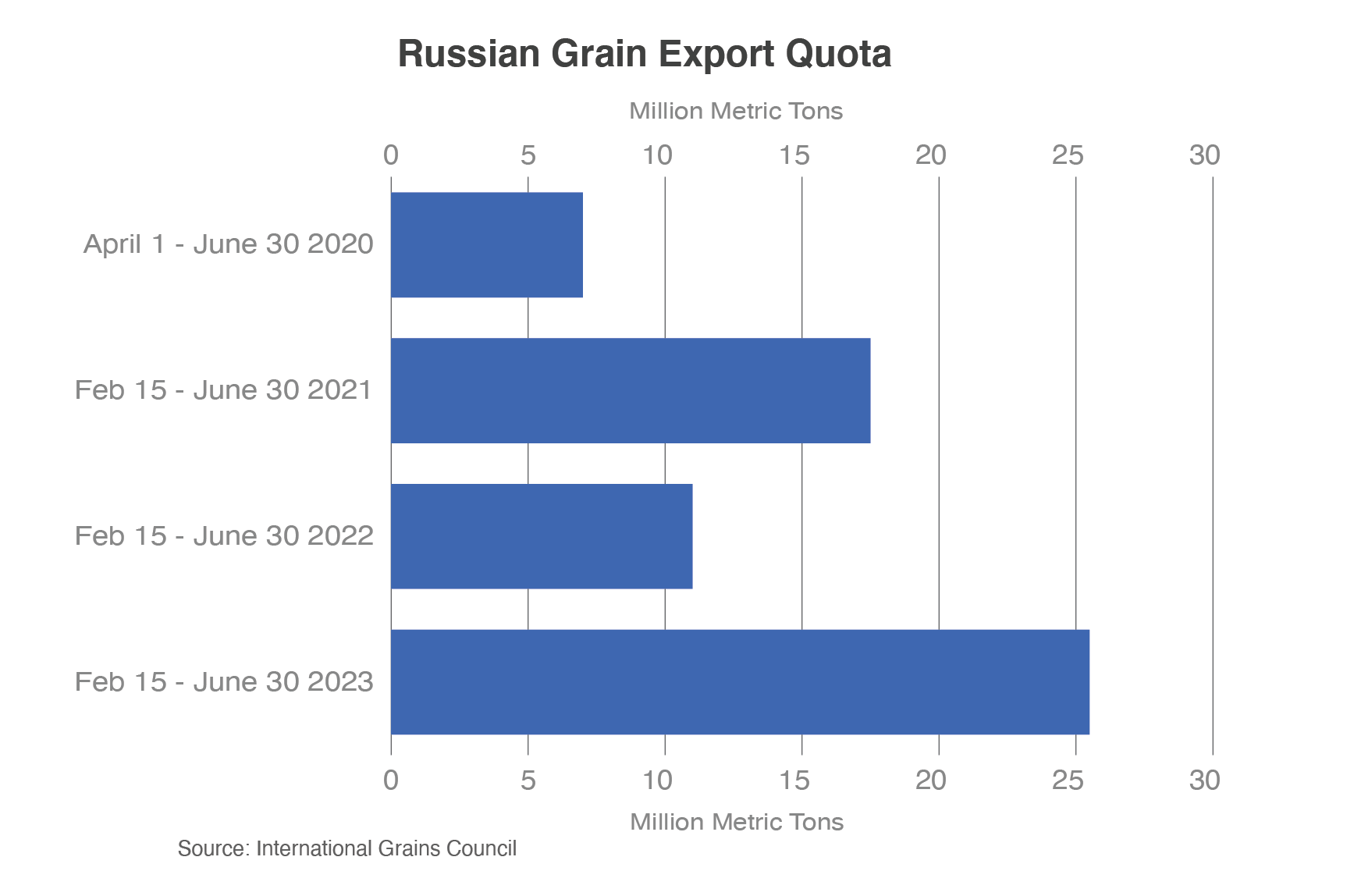

In recent years, Russia has also constrained volumes of agricultural exports through export quotas. A decade ago, Russia would simply ban its exports when there were reduced crops, but has since shifted to limiting export quantities, particularly in the latter half of the marketing year. What began as a policy implemented to dampen domestic food price inflation during the COVID-19 pandemic has become an annual occurrence. This policy is directly responsible for constraining exporters’ shipments. The quota has been adjusted on an annual basis to account for the available supplies; a smaller quota was issued during 2021/22 when Russia had a much smaller crop, and the quota was expanded in 2022/23 after a record crop was harvested.

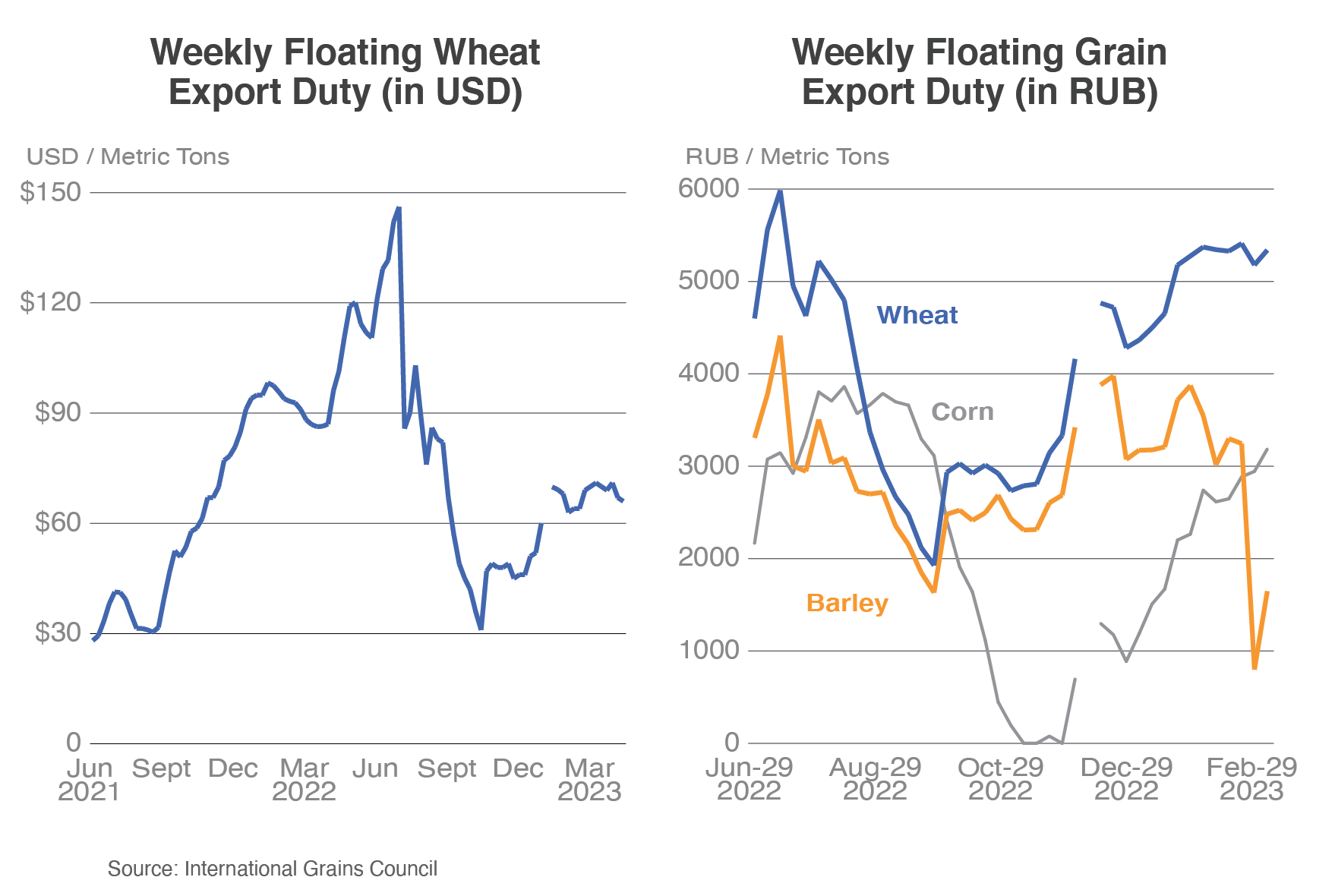

In 2021, Russia introduced an export tax aimed at quelling the rising food price inflation. The wheat export tax began in February 2021 at 25 euros/ton, rose to 50 euros/ton in March, and was converted to a floating export tax in June, calculated and announced on a weekly basis. The tax was $28.10/ton in June 2021 and peaked at $146.10/ton in late June 2022, prior to the harvest of its record 2022/23 crop. In July 2022, the methodology was updated, and the currency was denominated in rubles. For ease of viewing the relative prices, the chart on the left shows the continuation of the series with the tax converted to dollars. The chart on the right shows the wheat export tax in rubles relative to the taxes imposed on barley and corn. While Russia’s export tax has briefly dipped to zero for corn, it has remained non-zero for wheat and barley and ultimately must be factored into transactions with foreign buyers.

Beyond these grains, Russia has imposed other constraints for oilseeds including a partial export ban for rapeseed exports, with exemptions only for the region bordering China. The export tax for soybeans is 20 percent with a minimum of $100/ton, and is in place through the end of August 2024 in an effort to stimulate more domestic processing. As of March 2023, the sunflower oil export duty is 2,068 rubles/ton, roughly equivalent to $28/ton, while the sunflower meal export duty is 3,357 rubles/ton, approximately $45/ton.

Export taxes have a couple of impacts, creating a wedge between producer and export prices. Application of an export tax translates into higher export prices than would otherwise be observed. On the other hand, producers face lower returns with an export tax in place, and this in turn can reduce incentives for planting.

Summary

Throughout 2022/23, Russia has benefited from large supplies, both beginning stocks and record production. Russia has exported significant quantities of both grains and oilseeds, despite its lack of transparent trade data. Additional sources of data validate the strong export volumes amid low prices. Nevertheless, Russia continues to apply trade-restricting measures such as quotas and taxes without which exports could be larger.