Reviewing the Tariff-Rate Quotas for U.S. Beef Imports

Contact:

Link to report:

Executive Summary

The United States is the world’s largest producer of beef and its second-largest importer. Imports mostly consist of lean trimmings used for processing into ground beef. These trimmings, which would otherwise go toward rendering or pet food, add value to the U.S. beef supply chain. Beef imports usually follow the U.S. cattle herd cycle where a contraction leads to an increase in imports and vice versa. For beef imports, the United States established several World Trade Organization (WTO)-negotiated tariff-rate quotas (TRQs). The United States established TRQs for specific countries and gave remaining countries access to an “Other Countries” TRQ. Several countries have gained access to the U.S. market in recent years, thus increasing the competition within the “Other Countries” TRQ. Nevertheless, U.S. beef imports consist of mostly products from free trade agreement (FTA) partners.

Background on U.S. Beef Trade and Cattle Herd

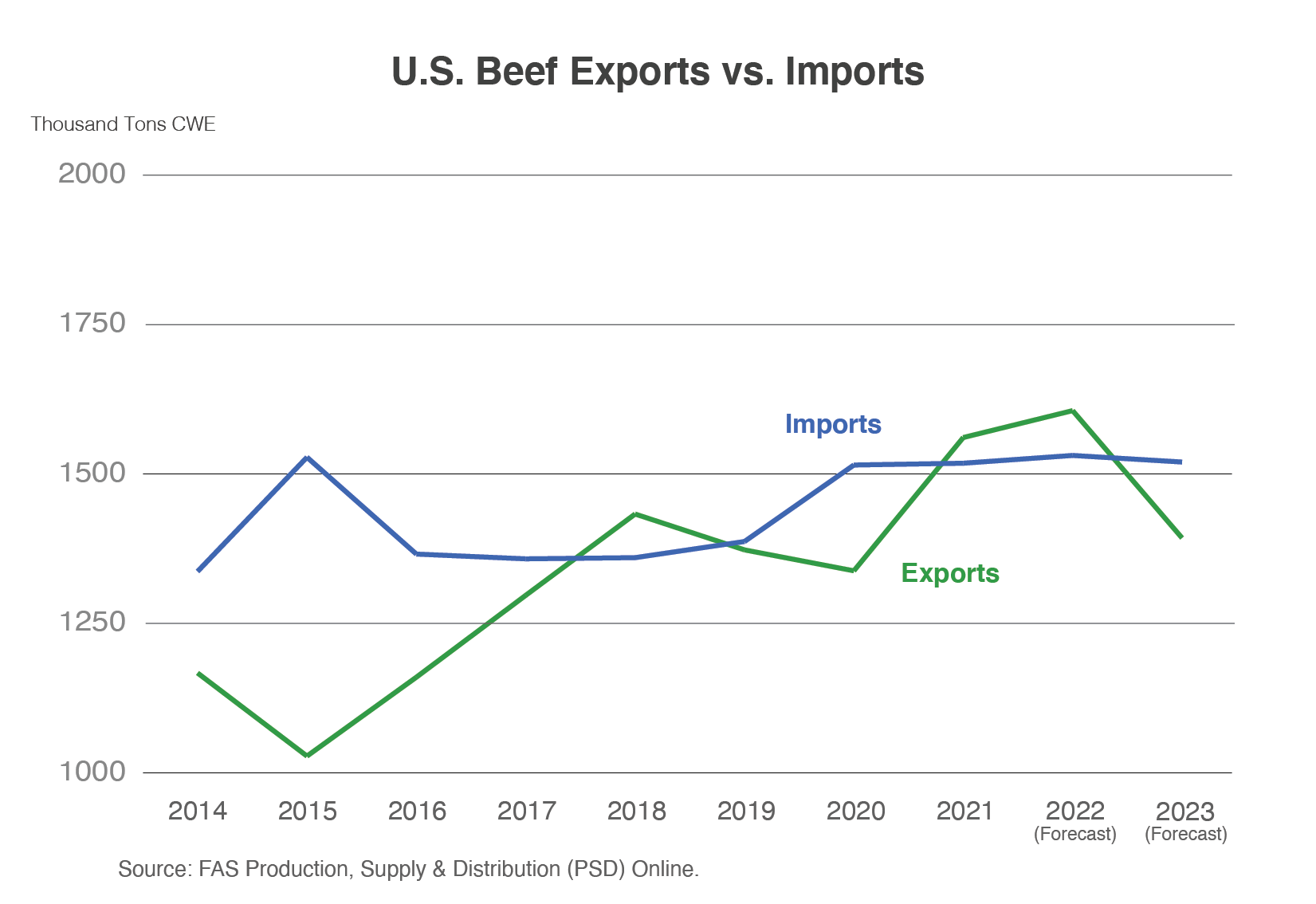

The United States is the highest beef producer globally, but it is also the second-largest importer. Overall, imports accounted for 10 percent of total U.S. beef supply in 2021. U.S. producers specialize in raising grain-fed cattle, which yields beef that commands the highest exports by value in the world. Conversely, most imports consist of lower-value, grass-fed lean “trimmings”— fat and muscle tissue remaining after processing a carcass. Because of U.S. cattle’s grain-fed diet, domestically produced trimmings require lean product to balance its high fat content and achieve the proper lean-to-fat ratio for making ground beef. As a result, these beef imports add value to U.S. producers. According to the USDA's National Agricultural Statistics Service (NASS) Cattle Inventory Survey, the U.S. beef cattle herd began contracting in 2019, falling from 31.69 on January 1, 2019, to 31.34 million head on January 1, 2020. Consequently, NASS’s January 1 survey shows the U.S. calf crop falling as well since 2019, leading to a decline in the overall herd size, which has continued into 2022. Meanwhile, high retail prices, firm consumer demand, and drought conditions in the Southern Plains have spurred additional cattle slaughter which reduced stocks of replacement heifers and beef cows. Despite fewer slaughter cattle on hand, the United States continued to be a net exporter of beef muscle cuts in 2021. This trend is expected to continue in 2022, but not in 2023 as tighter supplies begin to catch up with beef exports. In 2022, beef import1 pace has slowed from its record first quarter. High cow slaughter rates and large cold storage inventories have since bolstered domestic beef supplies. Nevertheless, 2022 beef imports are projected to be the highest since 2005. Thus far in 2022, the United States is exporting more beef on a volume basis, and is expected to remain a net exporter. In 2023, tighter cattle supplies will reduce exportable supplies, preventing further growth.

Suppliers and Basis for TRQ

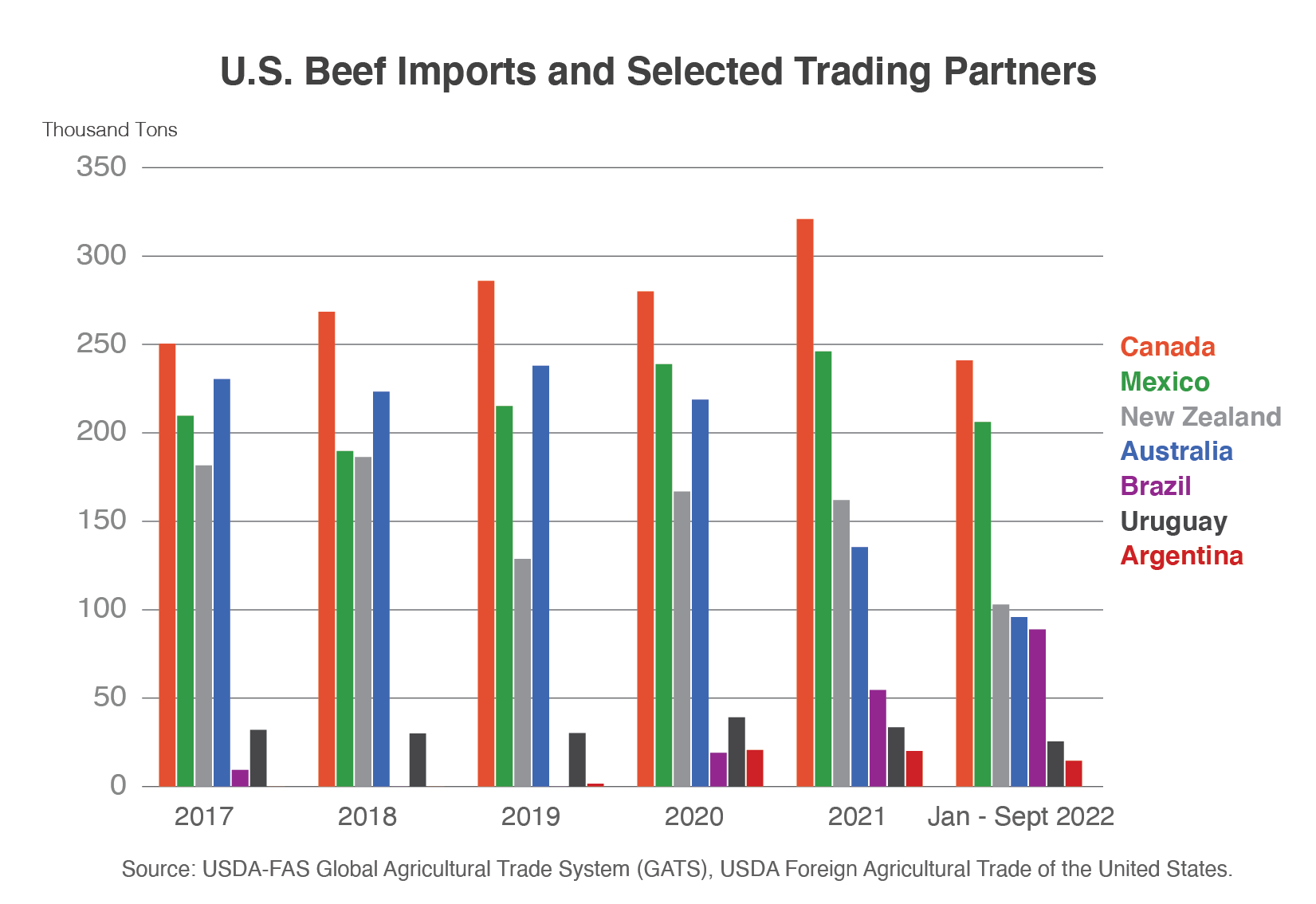

Since 2017, Canada has been the leading supplier of U.S. beef imports followed by Australia, New Zealand, and Mexico. In 2020, Mexico became the second-largest supplier to the United States and supplanted Australia amid the latter’s ongoing herd rebuild. Australia and New Zealand have historically supplied most imported beef trimmings to the United States; however, Brazil has recently made substantial gains in the U.S. market. Notably, Brazil lacks both a country-specific quota and a FTA with the United States. Therefore, Brazil competes within the “Other Countries” quota (65,005 tons). Countries subject to this TRQ include those which are (1) eligible to export fresh and frozen beef to the United States, (2) do not have their own country-specific quota, and (3) do not have a FTA with the United States.2

Sanitary Requirements for U.S. Beef Imports

Currently, 17 countries are eligible to export fresh and frozen beef to the United States: Argentina, Australia, Brazil, Canada, Chile, Costa Rica, the Dominican Republic, France, Ireland, Japan, Mexico, Namibia, Netherlands, New Zealand, Nicaragua, the United Kingdom, and Uruguay. Obtaining U.S. beef market access is a multi-step process. Countries must first be approved by the Animal and Plant Health Inspection Service based on animal disease status and the risk of disease introduction from trade. In addition, the Food Safety Inspection Service (FSIS) certifies that foreign food regulatory systems employ equivalent sanitary measures to U.S. standards.

| TRQ Countries and Report Dates | Report date | Tariff-rate Quota | Quota Fill-Rate | Rate of Duty | |||

| 11/1/2021 | 10/31/2022 | In-Quota | Above-Quota | ||||

| Product weight (metric ton) | |||||||

| TRQ countries | 328,736 | 311,945 | 696,821 | 45% | |||

| Australia | 110,794 | 106,015 | 378,214 | 28% | 0% | 21.1% | |

| New Zealand | 144,769 | 108,000 | 213,402 | 51% | 4.4 cents/kg | 26.4% | |

| Argentina | 12,613 | 16,225 | 20,000 | 81% | 4.4 cents/kg | 26.4% | |

| Uruguay | 16,225 | 16,807 | 20,000 | 84% | 4.4 cents/kg | 26.4% | |

| "Other" | 44,335 | 64,897 | 65,005 | 100% | 4.4 cents/kg | 26.4% | |

| Total | 298,799 | 291,691 | - | - | - | - | |

Sources: USDA, Economic Research Service, and U.S. Customs and Border Protection.

U.S. WTO TRQs

In the 1994 WTO Uruguay Round Agreement, the United States adopted a system of TRQs for imports of beef. The quota sets a volume limit for the calendar year. A lower rate of duty applies to product which enters the United States lower than the volume limit. For imports above the volume limit, a higher tariff applies. WTO negotiations resulted in several country-specific TRQs as well as the “Other Countries"3 TRQ. TRQ allotments were based on the level of historical imports from a given country. On a country basis, Australia and New Zealand received the largest quotas followed by Argentina and Uruguay.

Brazil’s Entrance Into the TRQ

The table above displays TRQs for country-specific and “Other Countries” quotas. In addition, it details the quota fill rate through June 6 of 2021 and 2022. Brazil’s use of the “Other Countries” quota accelerated the pace of its fill rate year-on-year.4 Brazil is the largest beef exporter within the “Other Countries” quota, and its shipments have occupied more than 90 percent of the TRQ. Brazil began exporting to the U.S. market in 2017, but sanitary concerns resulted in Brazil losing access from 2018 to May 2020. After detecting a case of atypical bovine spongiform encephalopathy in September 2021, Brazil lost access to its primary market, China, and shifted its focus to the United States. Brazil became the largest beef supplier between January and March of 2022.

The “Other Countries” TRQ filled in early April, but through September, Brazil continues to be the fifth-largest supplier of imported beef this year behind Canada, Mexico, New Zealand, and Australia. When considering all beef products (including those not subject to the TRQ), Brazil becomes the third-largest supplier this year. Brazilian product has remained competitive despite incurring the out-of-quota duty due to high U.S. beef prices, firm demand for manufacturing beef, and limited global competition. Australia and New Zealand, the other major beef trimmings exporters to the United States, have faced several challenges in recent years regarding their processing sectors. COVID-induced labor constraints caused slaughterhouses to operate below capacity in both countries. Meanwhile, disastrous floods around Brisbane in March 2022 further stunted beef exports. Therefore, between January and June, Brazil displaced Australia and New Zealand as the third-largest U.S. market supplier.

FTAs: Past and Present TRQs

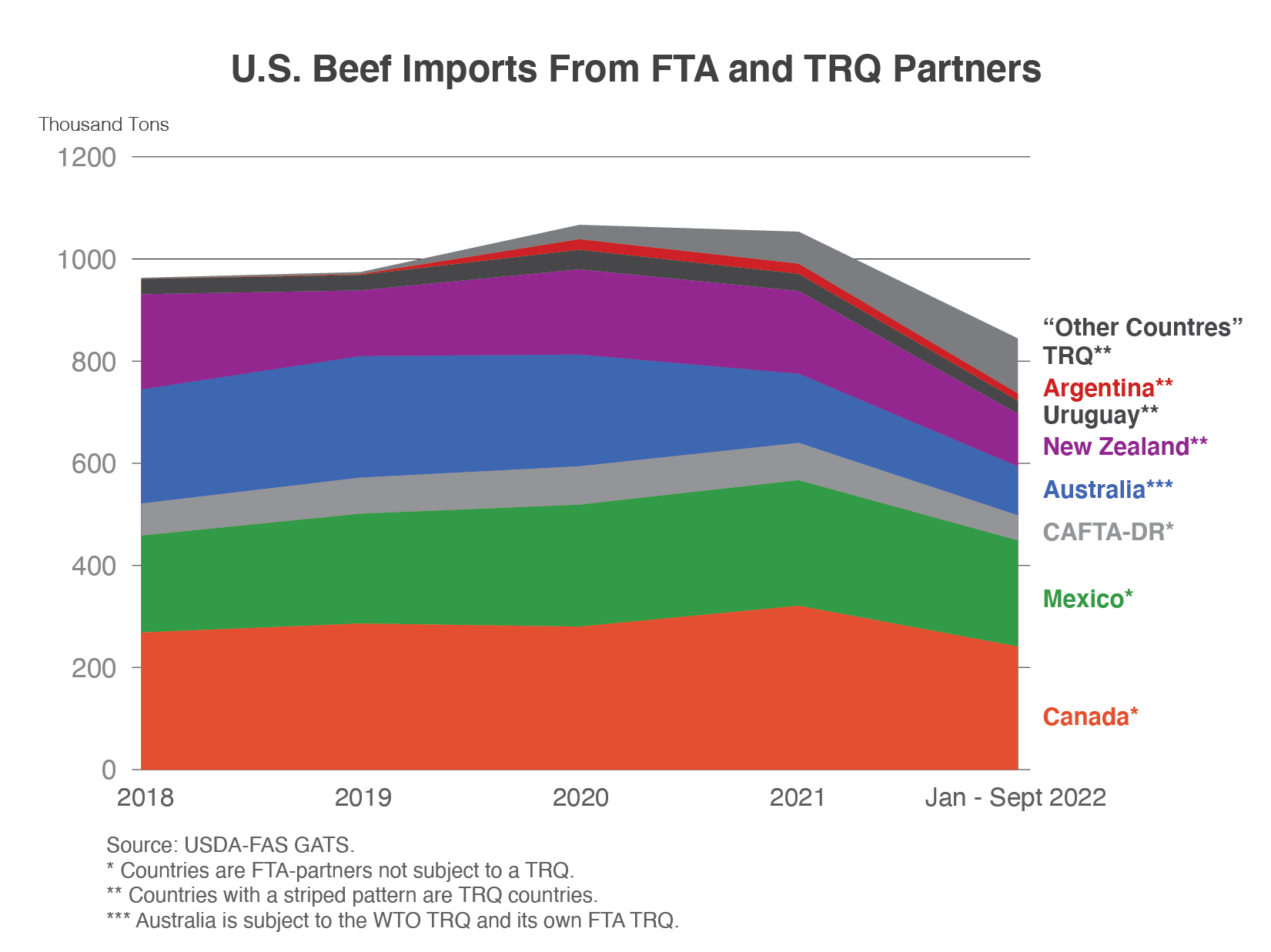

United States-Mexico-Canada Agreement (USMCA): Replaced the North America Free Trade Agreement (NAFTA) and has been in effect since 2020. Canada and Mexico previously received duty-free access from NAFTA, and USMCA maintains the status quo. Between 2017 and 2021, Mexico and Canada supplied on average 48 percent of beef to the United States.

U.S.-Australia FTA: In addition to its WTO quota, Australia has another country-specific quota through its own FTA in effect since 2005. In 2023, Australia will enjoy duty-free access as excess-quota duties are phased out.5

Dominican Republic-Central America Free Trade Agreement (CAFTA-DR): The United States allowed duty-free access to CAFTA-DR members in 2021. Prior to 2021, CAFTA-DR countries eligible to export beef to the United States received individual TRQs if the “Other Countries” TRQ was filled. Costa Rica and Nicaragua are currently the only member countries which actively export beef to the United States. The Dominican Republic received eligibility in 2022 and is expected to start exporting to the United States in 2023. Meanwhile, Honduras is still pending reinstatement by FSIS.

U.S.-Chile FTA: The United States had a specified quota limit for Chilean beef imports for 3 years after the FTA went into effect in 2004. Currently, Chile’s beef exports to the United States enter duty-free.

U.S.-Japan Trade Agreement (USJTA): Prior to the USJTA, Japan possessed its own TRQ of 200 tons. However, as part of the agreement which began in 2020, Japan petitioned for access to “Other Countries” TRQ in exchange for giving up its own TRQ.

Other FTA TRQs: The United States also allows duty-free access for beef imports from Bahrain, Colombia, Morocco, Oman, Panama, and Singapore. However, none of these countries are currently eligible to export beef to the United States.

Quota Arrangements

Any changes to the WTO TRQ quantities or country allocations would require negotiations through the WTO. Similarly, changes to FTA quotas or country allocations necessitate negotiations between the United States and the partner country. In most cases, an FTA quota phases out after a certain timeframe. FTA partners account for most U.S. beef imports. Meanwhile, TRQ trading partners send product on a first-come, first-served basis, but others (New Zealand and Australia) allocate permits to individual exporters. The “Other Countries” quota is on a first-come, first-served basis.

Looking Ahead: U.S. Beef Imports in 2023

According to the NASS January 1 Inventory Survey6, the U.S. cattle herd continues to contract in 2022. Both higher slaughter rates and cattle on feed through September 2022 further reinforce that the U.S. cattle herd will continue its contraction into 2023. Beef imports historically remain elevated as the supply of slaughter-ready cattle dwindles and beef production wanes. This trend is expected to continue amid a forecasted herd contraction in 2023. Brazil and Canada have become the United States’ top suppliers for beef trimmings amid Australia and New Zealand’s pullback from the U.S. market. However, U.S. imports from Australia are expected to rebound from historic lows. In 2023, duty-free access, an improved labor situation, and greater cow slaughter will help propel Australia’s reemergence in the U.S. trimmings market. FSIS is evaluating several prospective exporting countries7 to determine equivalency for beef imports which means competition for the “Other Countries” quota could increase in the future. Nevertheless, Brazil’s production capacity far exceeds that of its competitors in the “Other Countries” TRQ. As a result, Brazil may remain the largest “Other Countries” TRQ contributor. Any future changes to U.S. import quotas would require WTO or FTA negotiations, depending on the quota’s origin.

1 Beef imports include fresh, chilled, and frozen muscle cuts from HS headings 0201 and 0202 and exclude processed, offal, and prepared products which are not subject to U.S. TRQs.

2 Table compiled from ERS and CBP data: https://www.ers.usda.gov/data-products/livestock-and-meat-international-trade-data/.

3 These countries currently are Brazil, Ireland, Japan, Namibia, the U.K., France, and the Netherlands.

4 While the “Other Countries” quota does not show the full allotment as filled, the quota is full. Some beef products which came in less than quota were later found to be ineligible for import. Therefore, this quota “space” was filled but not actually imported into the U.S., resulting in the discrepancy.

5 For more information on the phase-out of Australia’s FTA TRQ duties, please see: https://www.dfat.gov.au/trade/agreements/in-force/ausfta/fact-sheets/Pages/agriculture.

6 NASS Cattle Survey: https://www.nass.usda.gov/Surveys/Guide_to_NASS_Surveys/Cattle_Inventory/.

7 For the list of countries which FSIS is in the process of examining (updated monthly), please see: https://www.fsis.usda.gov/sites/default/files/media_file/2022-04/equivalence-status-chart.pdf.